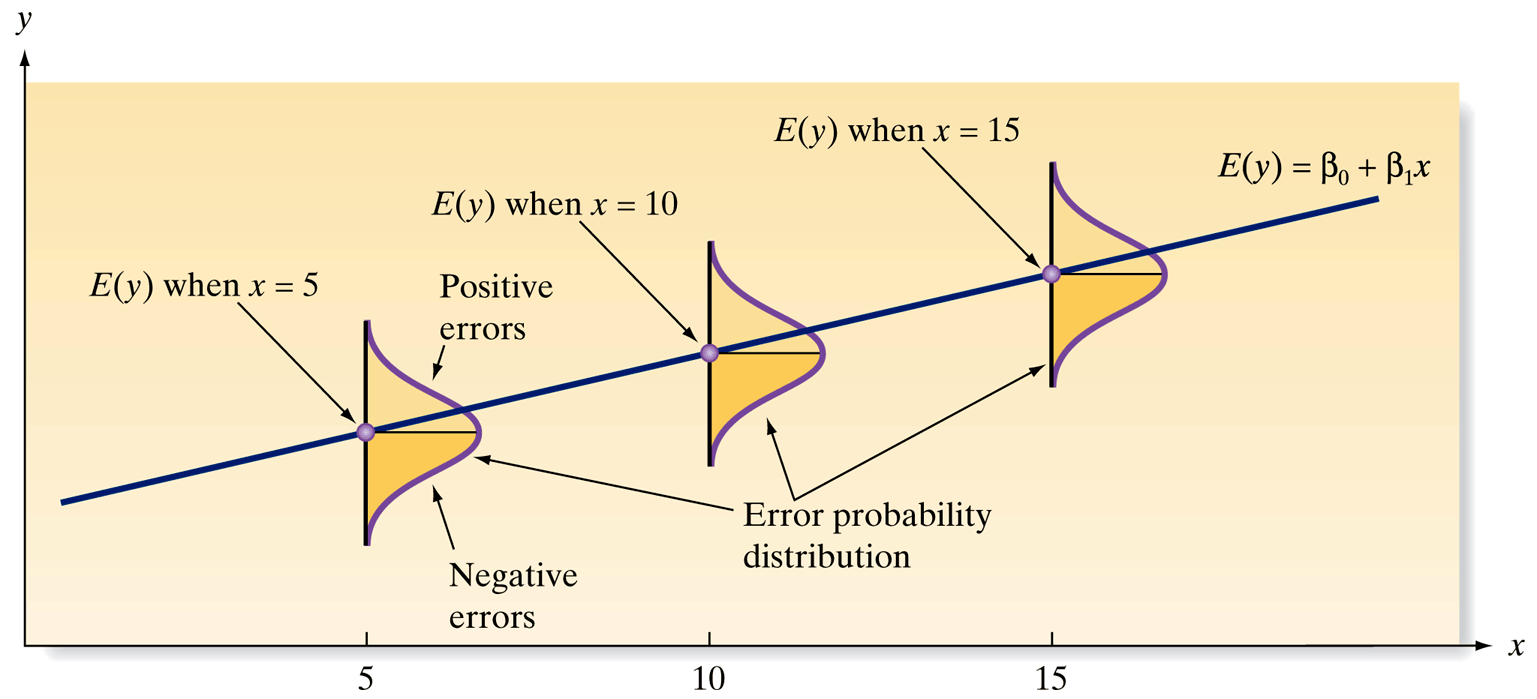

Mean of Errors (\(\varepsilon\)): The mean of the probability distribution of \(\varepsilon\) is 0, aligning the expected value of \(y\) with \(\beta_0 + \beta_1 x\) for any \(x\).

Constant Variance: The variance of \(\varepsilon\) is constant across all values of \(x\), denoted as \(\sigma^2\).

Normal Distribution of Errors: \(\varepsilon\) follows a normal distribution.

Independence of Errors: The errors associated with different \(y\) values are independent.

Constant Variance

# Define the datax <-c(1, 2, 3, 4, 5)y <-c(1, 1, 2, 2, 4)# Fit a linear modelmod <-lm(y ~ x)summary(mod)

Call:

lm(formula = y ~ x)

Residuals:

1 2 3 4 5

4.000e-01 -3.000e-01 6.478e-17 -7.000e-01 6.000e-01

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.1000 0.6351 -0.157 0.8849

x 0.7000 0.1915 3.656 0.0354 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.6055 on 3 degrees of freedom

Multiple R-squared: 0.8167, Adjusted R-squared: 0.7556

F-statistic: 13.36 on 1 and 3 DF, p-value: 0.03535

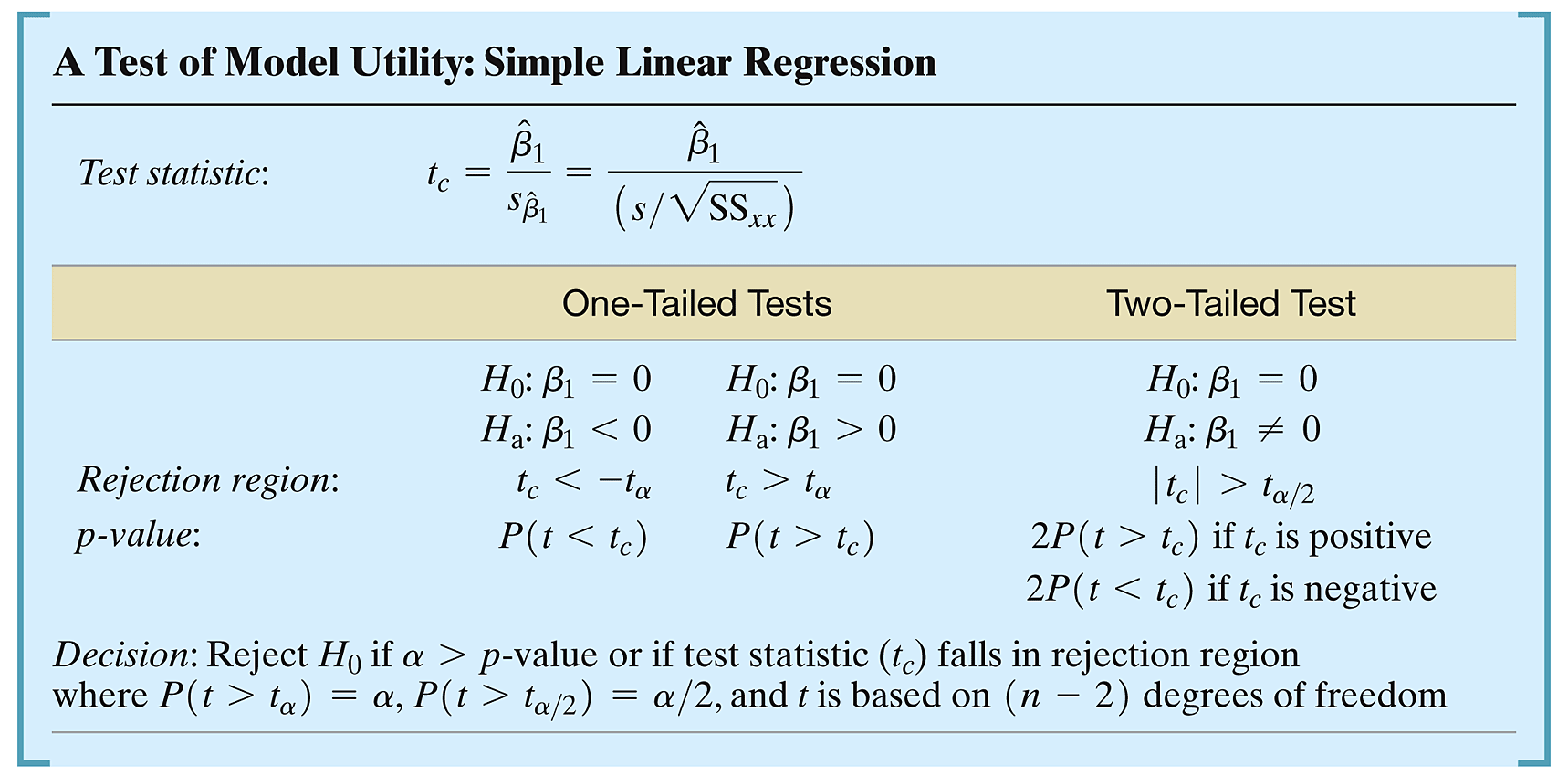

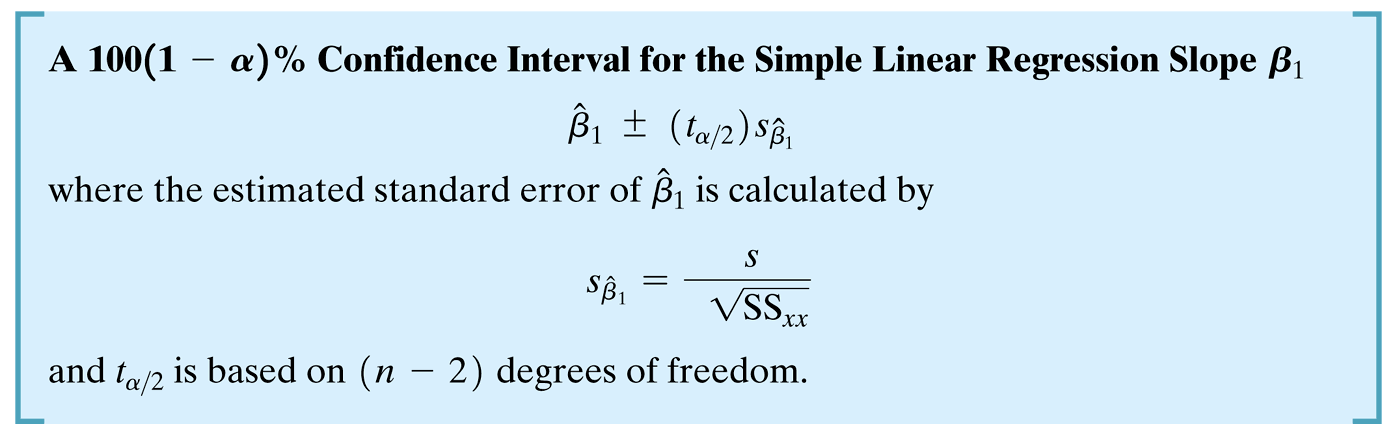

Making Inferences About the Slope \(\beta_1\)

Objective: Assess the significance of the slope \(\beta_1\) to understand the contribution of \(x\) in predicting \(y\).

Statistical Test:

Null Hypothesis (\(H_0\)): \(\beta_1 = 0\) (No relationship)

Alternative Hypothesis (\(H_a\)): \(\beta_1 \neq 0\) (Significant relationship)

Using R for Hypothesis Testing:

Perform t-tests to decide whether to reject \(H_0\). A significant \(p\)-value (\(< \alpha\)) indicates a meaningful contribution of \(x\) to predicting \(y\).

Practical Steps Using R

Conducting the Test:

Estimate \(\hat{\beta}_0\) and \(\hat{\beta}_1\) using the least squares method.

Compute the standard error and perform a t-test to check the significance of \(\hat{\beta}_1\).

Interpret the results: A significant test suggests that changes in \(x\) systematically relate to changes in \(y\).

Hypothesis Testing

How can we make a decision of this hypothesis test using R?

Estimate

Std. Error

t value

Pr(>|t|)

(Intercept)

-0.1

0.6350853

-0.1574592

0.8848840

x

0.7

0.1914854

3.6556308

0.0353528

Confidence Intervals

Confidence Intervals in R

confint(mod, level =0.95)

2.5 % 97.5 %

(Intercept) -2.12112485 1.921125

x 0.09060793 1.309392